1. Org info: tell Synscribe who you are

Your Organization Information is the top-level context every part of Synscribe reads: what you do, what you sell, and your regulatory posture. Make it accurate and specific. For a regulated business, spell out what you are and aren’t (for example, “a licensed payments institution, not a bank or lender”). This shapes how Pi writes and gives the guardrail the context to judge claims correctly.2. Product Bible: bound your claims

The Product Bible is Pi’s source of truth about your company, kept in its memory. Its Impact Claims section carries the rule “every number needs a source; never invent metrics,” and you flag up front what must not be claimed: specific metrics, customer names, positioning, or regulatory language that’s off-limits. That list becomes the input to every layer below.3. Landing-page pillar prompt: constrain what gets written

Bake non-hallucination hard rules into your pillar prompts: do not invent metrics, certifications, customer names, or capabilities. When you set up a pillar, Pi asks up front what must not be claimed and writes those constraints into the prompt, so generation never produces the forbidden claim to begin with.4. Refiners: auto-fix drafts before they’re judged

Refiners rewrite each draft to match your brand and compliance rules, at generation or on demand, so most issues are fixed before the guardrail ever sees the draft. Refiners run before the guardrail (see refiner vs guardrail).5. Evals: gate what’s left

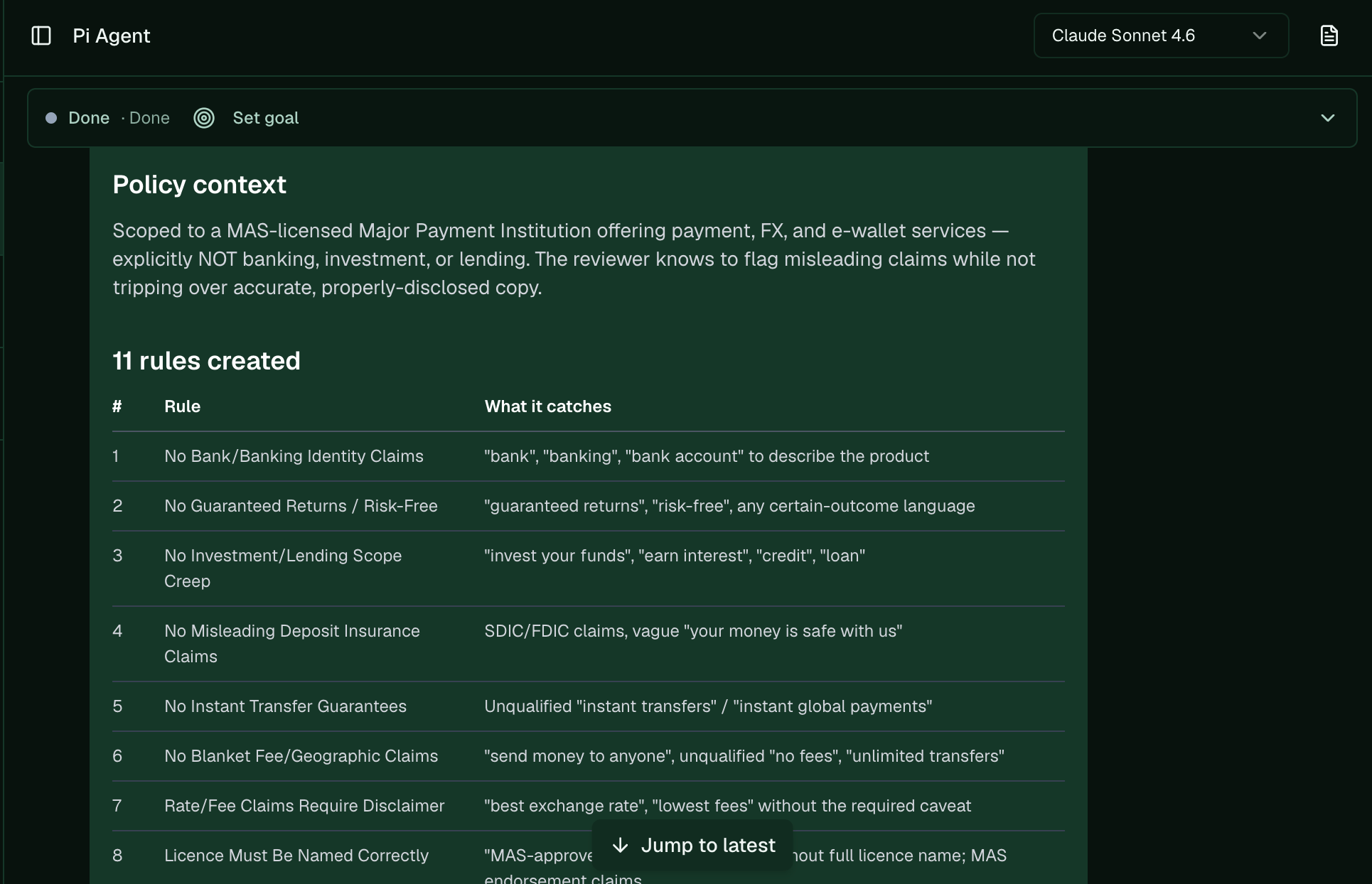

The compliance guardrail is the backstop. At publish it judges the finished piece and blocks anything that still breaches a rule. Write its rules to encode exactly what your business can’t say, each with a carve-out so it doesn’t over-flag, then calibrate it on copy you know should pass and should fail.A worked example: a regulated fintech

Take a fictional licensed fintech that issues a regulated digital-payment token. Its guardrail rules might read:| Rule | Flag | Carve-out (do NOT flag) |

|---|---|---|

| No guaranteed returns | Any promise of yield, returns, or profit | Factual statements about how the product works (e.g. that a balance is redeemable) |

| No regulator endorsement | Implying a regulator endorses or backs the product | Factual, accurate statements of the licenses actually held |

| No absolute safety claims | ”100% safe”, “risk-free”, “can’t lose” | Qualified statements tied to real reserves or audits with a source |